Monday 3rd of October 2022

Listen to this financial market update by playing this audio...

This week, we continue our series on the likely catalysts for the next bull market...

It's important to recall that throughout 2022, and especially in recent months, Dominion Capital Strategies has reiterated their view that this current bearish cycle is not yet over, with more risks for investors. This will eventually end and a new bull market cycle will come for stock markets, the question is when and what will drive that sustained upward movement in stocks?

Last week we looked at Dominions first episode on "bull market catalysts" series, which includes a shift in central bank policy, and why this outcome would precipitate a new bull market cycle.

This week, the second episode of their catalysts series will explain why investors should understand what a sustained decline in inflation is.

Inflation levels remain stubbornly high around the world, near their highest readings in forty years. The wide rise in price levels is the ultimate cause of the current bear market cycle in asset prices. It was higher inflation that triggered central banks to raise interest rates and reduce market liquidity, an ongoing process that puts downward pressure on the prices of all assets.

This leads us to ask:

If there were a significant decline in inflation from here, what would that mean for markets and investors?

The answer is: it depends. It depends on the nature and causes of any decline in inflation. A significant supply-side response – that is, higher prices across the economy incentivize an increase in the supply of goods and services, thereby bringing prices back down, causing inflation to fall – would be a very positive outcome. This would certainly drive a new bull market cycle in stocks.

However, if from here inflation were to decrease because high prices destroy demand, acting as a brake on the rise in prices, the end result would be an economic recession, the decrease in corporate profits and the consequent fall of the stock markets. This result would prepare us for the next bull market cycle, given that it would still kill the inflation monster, but we would have to go through a recession first.

Which of the two is more likely? In Dominions opinion, probably a mixture of both. There will be a supply-side response to higher prices. A good example is here in the UK, where oil and gas drilling and production activity in the North Sea has increased to full capacity to produce as much energy as possible to supply the UK and Europe, in light of Russia's disconnect from its supplies to the continent. A similar activity will occur in all supply chains experiencing price increases.

At the same time, rising inflation and the consequent rise in interest rates are also destroying demand. We are seeing a significant slowdown in consumer demand in areas such as electronics, as well as clear evidence of the slowdown in the real estate market around the world. This, in turn, is reflected in a growing set of economic indicators that signal a possible recession.

The combination of these factors already translates into a drop in prices in many of the main inputs of the economy. Prices of most commodities have fallen sharply from the highs reached at the beginning of the year. Other input costs, such as freight and components, have also seen their prices fall from much higher levels in early 2022. Wage inflation remains positive, but it has not run rampant in the same way it did during the inflation cycle of the 1970s.

In real terms, the average worker in the U.S. and Europe has suffered a pay cut this year. Sharp rises in house prices in 2021 have stalled and in some places are being reversed. These are all leading indicators of official inflation data, meaning that we should start to see official inflation figures go down.

The timing of this is uncertain, inflation is slippery and has historically been incredibly difficult to predict, but there are reasons to be progressively optimistic that much of the inflationary pressures may begin to ease in the coming months. Now, it could be a slow process, with bumps in the road, but the direction of travel is becoming clearer, and that's good news for long-term investors.

When official inflation figures begin to fall steadily, this will be a strong catalyst for more stable equity markets and increase the likelihood that a new serious bull market cycle will begin. And we'll be the first to tell everybody. From here it requires patience on the part of investors, but we are getting closer and closer to the moment when we can call, with confidence, the next bull market cycle.

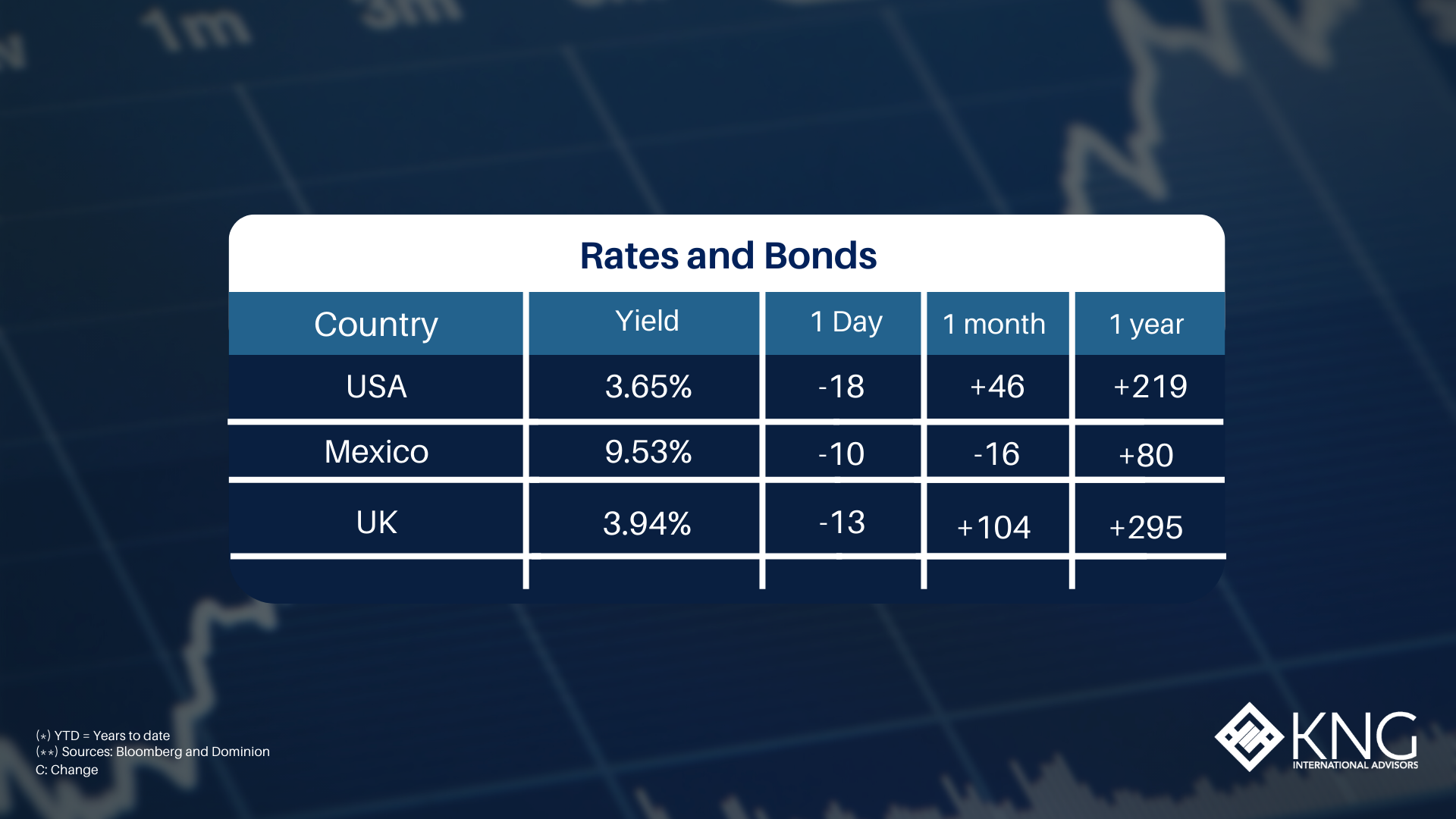

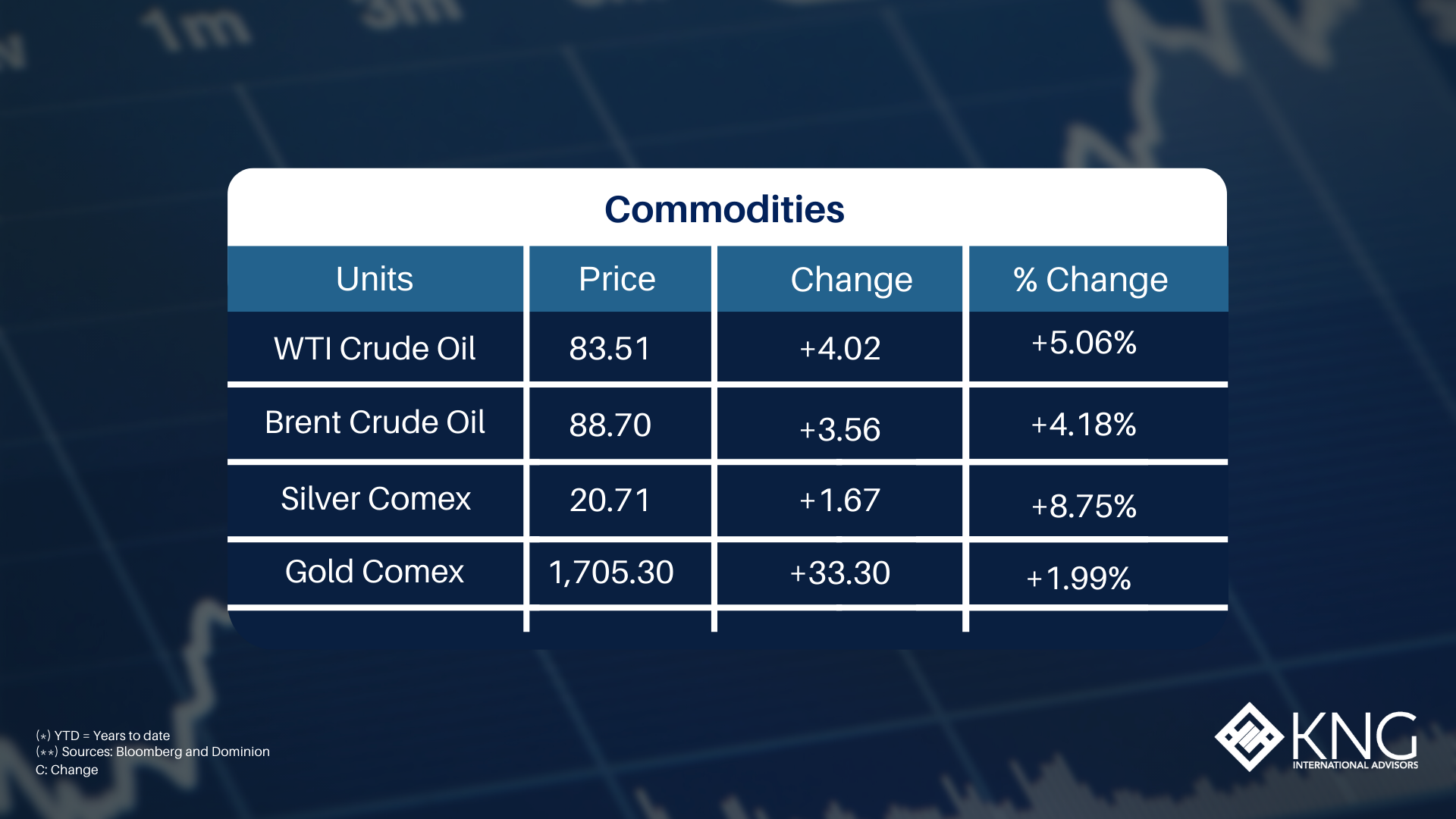

Sources: Bloomberg, Yahoo Finance, Marketwatch, MSCI. Copyright © 2021 Dominion Capital Strategies, all rights reserved.