Tuesday 11th of April 2023

Listen to this financial market update by playing this audio...

Skittish markets in the short term...

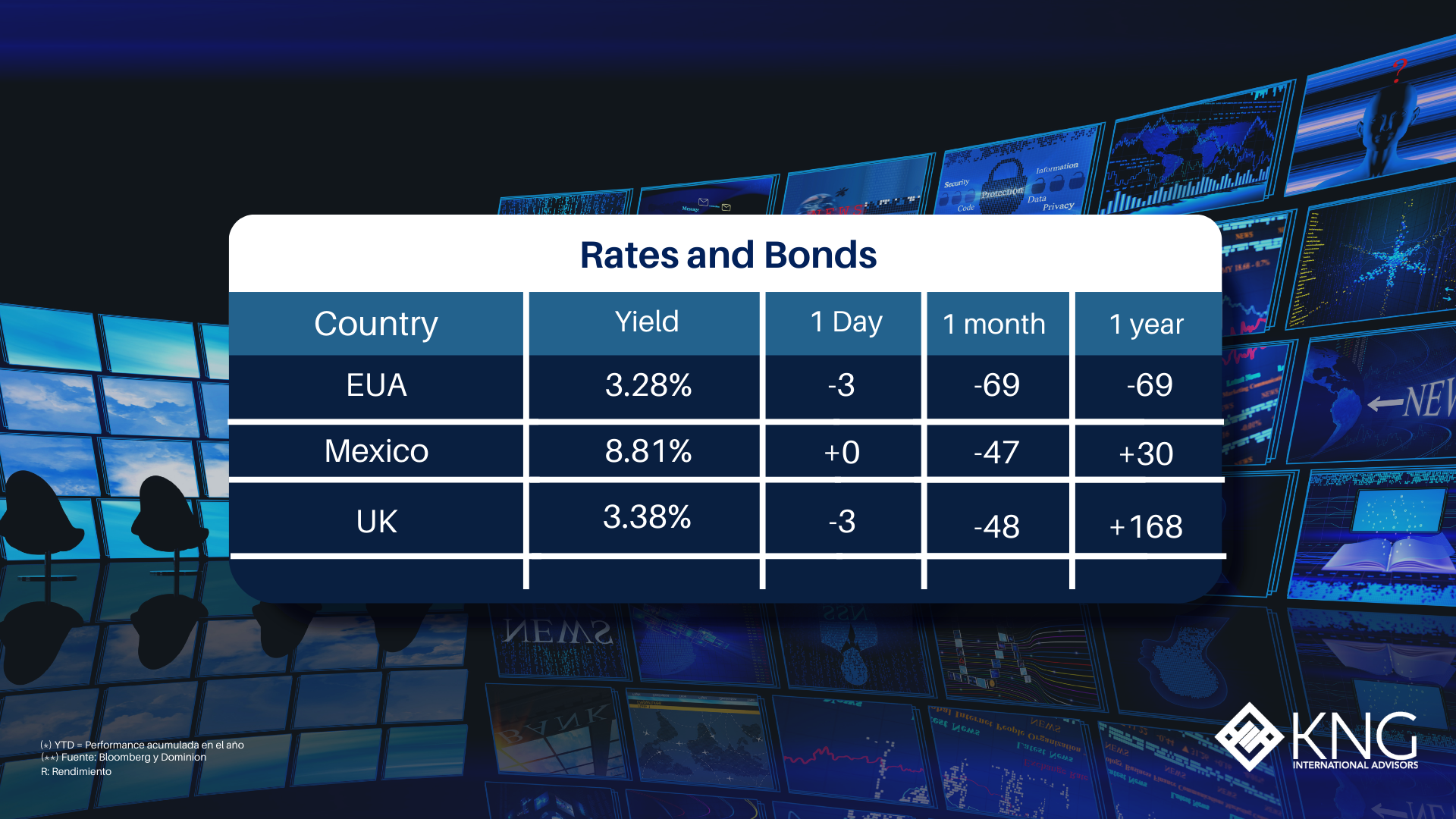

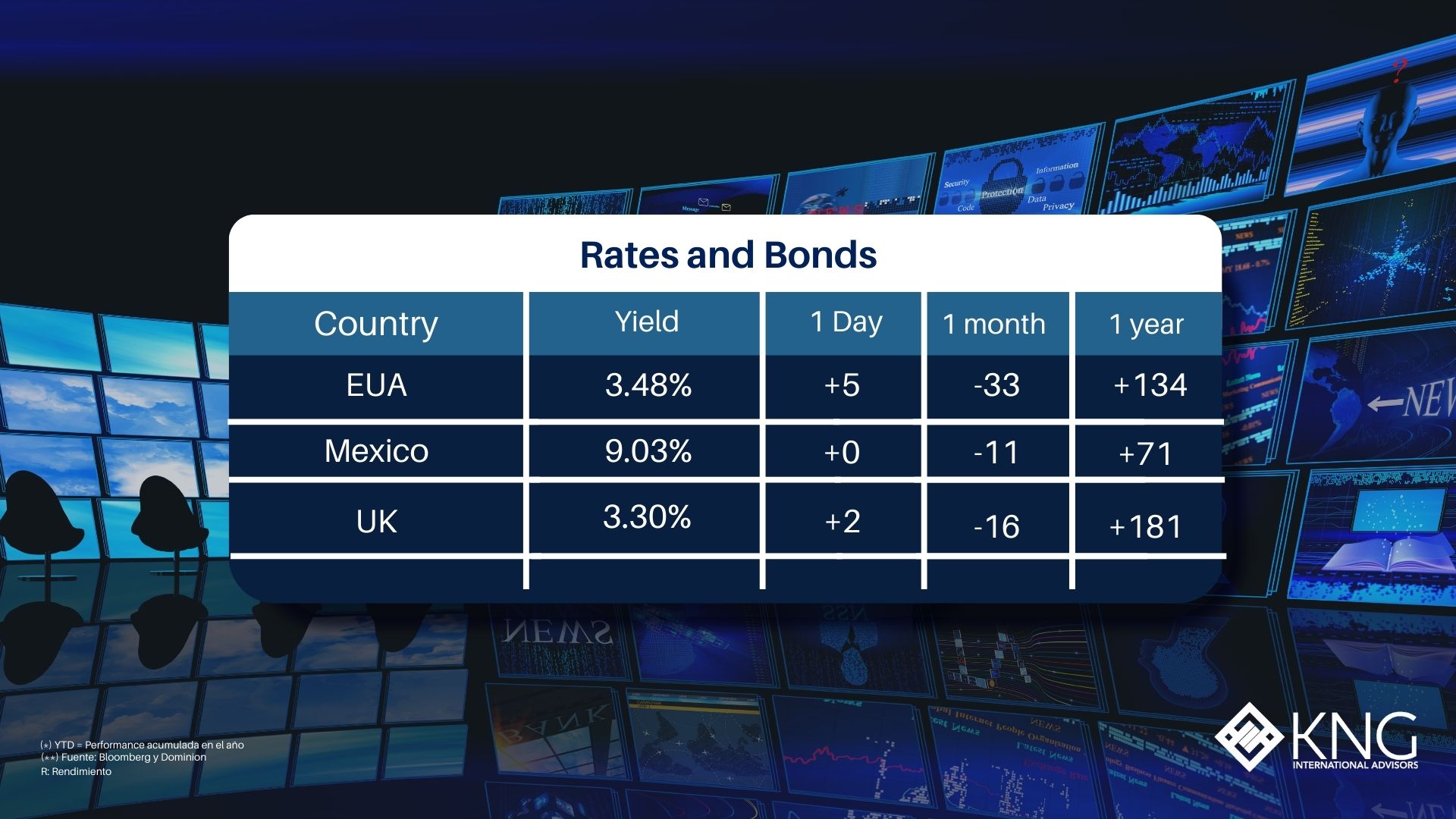

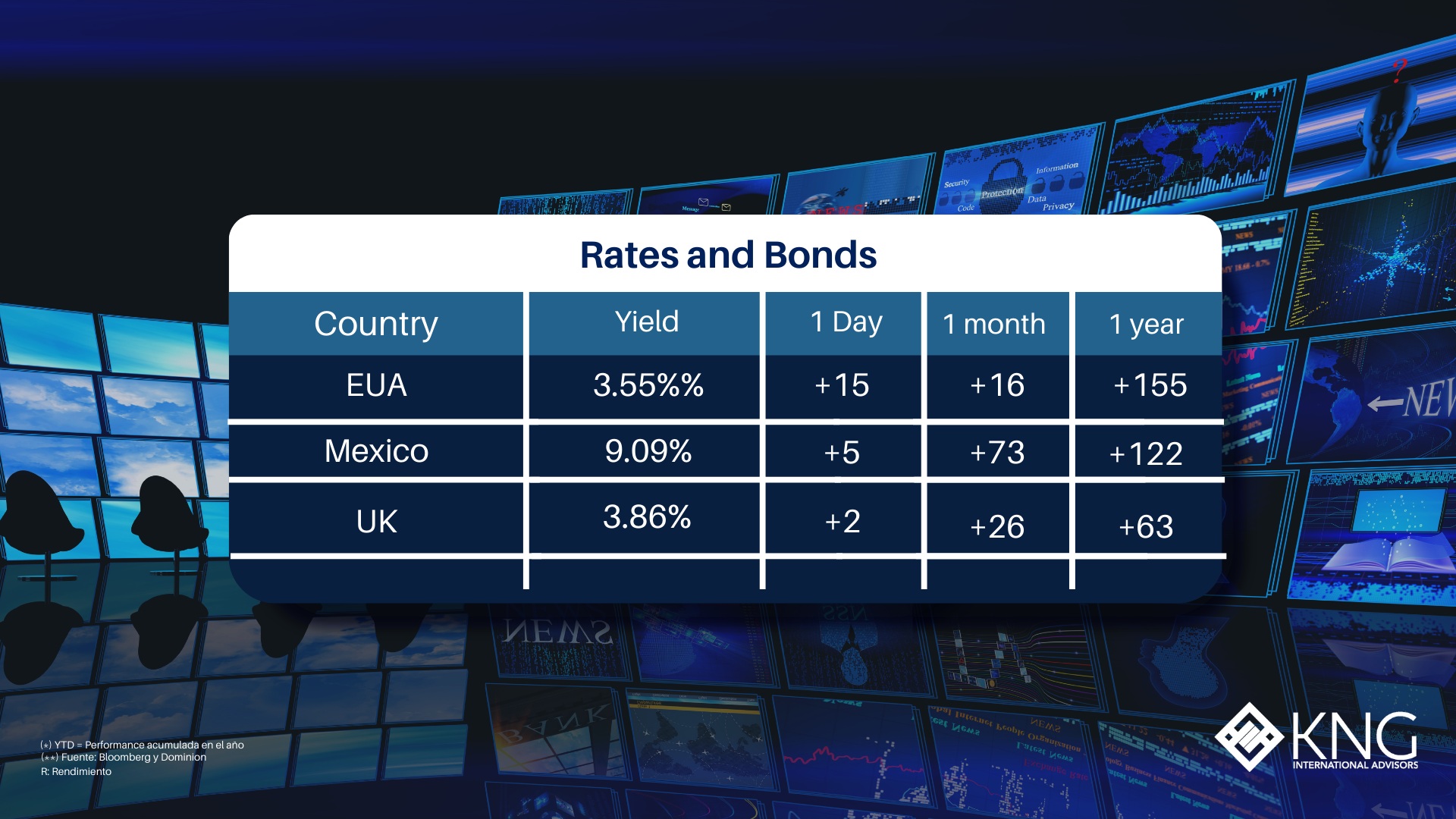

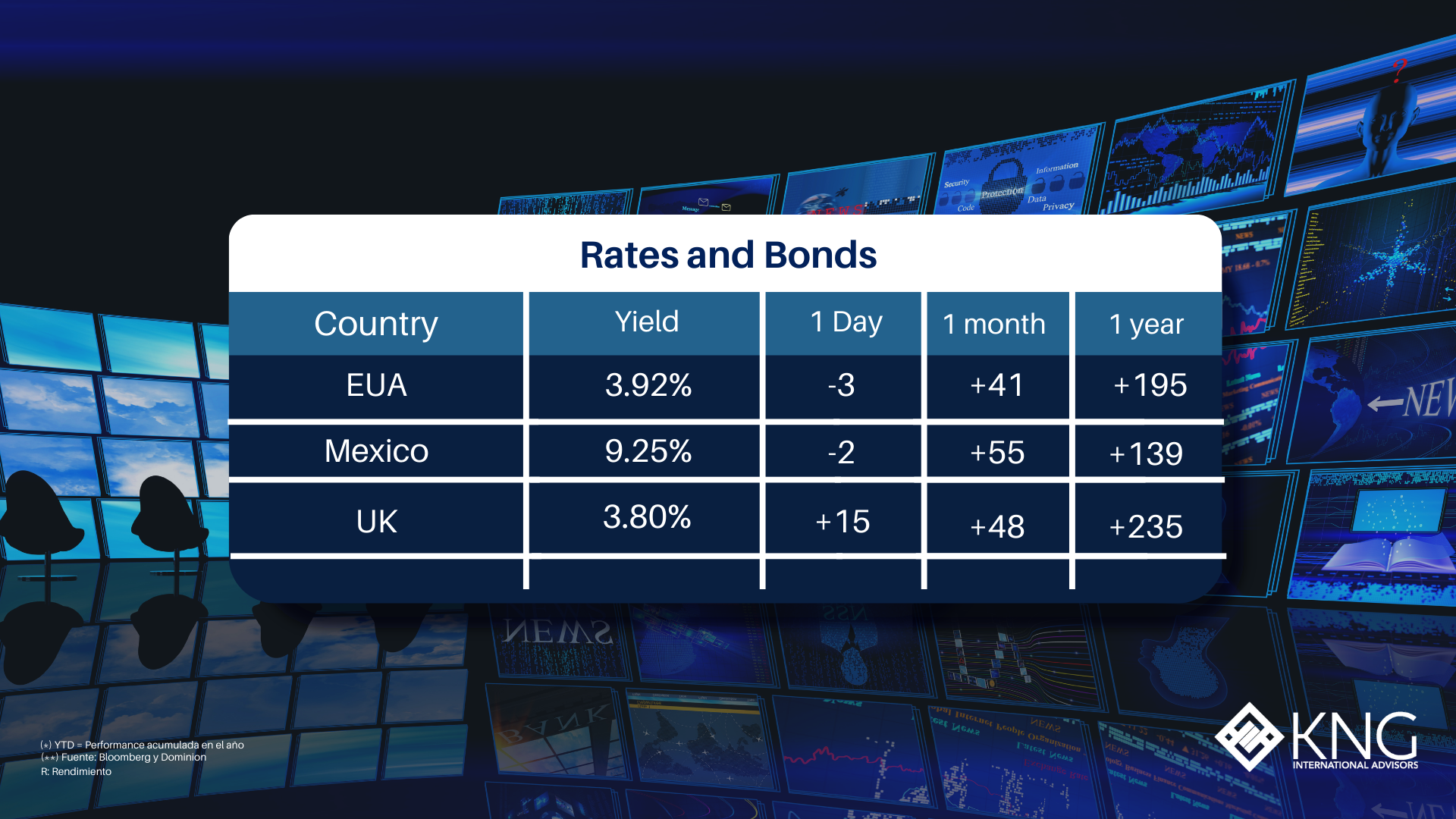

The current investment environment continues to be challenging, with trailing one-year returns for many asset classes remaining in negative territory. Despite the recent rally in equities, markets remain skittish with many market commentators calling for further volatility and potential downside for asset prices in the coming weeks / months.

We tend to agree that in the short-term we could see further weakness in markets, see our episode from last week for more information on our thinking there.

But as investors, it is the long-term that really matters. Despite the short-term uncertainty and risk of further bouts of market weakness, for the long-term minded investor there are some very attractively valued assets available today.

In some specific areas of the commodities (and related equities) market, we believe, there are interesting dynamics that could offer differentiated returns to a diversified portfolio in 2023 and beyond.

The current demand and supply outlook for some commodities is especially interesting, while the current market valuations offer a degree of a ‘margin of safety’ for investors.

It is rare in any industry to have very much visibility on what demand levels will look like 1-year, 2-years, or more into the future. All industries and markets are inherently difficult to forecast.

We do, however, have a unique starting point today in some sectors of the economy where we can make confident predictions of what demand is likely to look like.

Climate change and the energy transition away from fossil fuels to decarbonise the global economy is a multi-trillion-dollar, multi-decade, global investment opportunity that is already happening now and is set to accelerate. Major governments around the world are committing to major spending subsidisation programs to further accelerate this transition.

What does this mean in reality?

It means upgrading and replacing electricity grids across the planet, it means vast build outs of offshore wind farms and solar projects, it means major build outs of nuclear power plant fleets and the associated infrastructure to connect these new sources of power to the grid, it means hundreds of millions of batteries rolling off of production lines every year to power new fleets of electric vehicles.

What do these aspects of the energy transition have in common? They are all very heavy users of industrial metals, in particular, copper. Copper as a metal is unique in its heat and electricity conductivity, its relative cost, and performance as a material in applications like wiring or EV batteries. The energy transition is going to be very intensive in its use of copper.

Some industry estimates indicate we may need 2-3x the current global copper supply to meet the needs of the global energy transition over the coming 20 years.

When we look at the supply of this critical metal, however, we do not see anything like the expected increase in future supply coming online over the next 10-20 years to meet this major wave of demand.

Why is that?

Copper is a relatively scarce metal in mineable deposits. It has been a useful and widely used material by civilisation for thousands of years. This means the relatively easy to access mineable deposits of copper have largely been exhausted around the world.

Each incremental new mine to produce copper is harder to access, further away from transportation infrastructure, and therefore more costly to bring online.

This creates an interesting set-up for investors willing to invest in the few companies who own high quality mining assets in the copper industry.

We know with a high degree of certainty that demand for this material is going to go up. And it is going to go up a lot!

Meanwhile there are fundamental barriers to bringing on new supplies of copper, as outlined, which restricts the ability of the global industry to raise supply as quickly as demand is rising.

When demand for any good exceeds supply, prices rise. A structural rise in prices of any product or commodity is good news for the existing suppliers of that product. In this case, the structural rise in prices of copper, driven by the coming demand supply imbalance, will be very beneficial for the owners of copper producing assets.

While markets continue to lurch from blind optimism, to deep pessimism, and then back again, obsessed with changes in the short-term, we think it wise to think a little bit longer-term and consider allocations in portfolios with a multi-year, or even as in this investment case for copper, a multi-decade time horizon. It can certainly help investors sleep a little easier!

We would like to thank Dominion Capital Strategies for writing this content and sharing it with us.

Sources: Bloomberg, Yahoo Finance, Marketwatch, MSCI.

Copyright © 2023 Dominion Capital Strategies, All rights reserved.

Disclaimer: The views expressed in this article are those of the author at the date of publication and not necessarily those of Dominion Capital Strategies Limited or its related companies. The content of this article is not intended as investment advice and will not be updated after publication. Images, video, quotations from literature and any such material which may be subject to copyright is reproduced in whole or in part in this article on the basis of Fair use as applied to news reporting and journalistic comment on events.